What is the accounting standard 5

Accounting Standard 5 (AS 5) deals with the classification and disclosure of specific items in the Statement of Profit and Loss. The purpose of AS 5 is to suggest such a classification and disclosure in order to bring uniformity in the preparation and presentation of statement of net profit or loss across enterprises.

What is accounting standard 6

AS-6 deals with depreciation of the tangible asset. Hence, only the historical cost, accumulated depreciation on the asset and total depreciation for the period for each class of asset will be recorded.

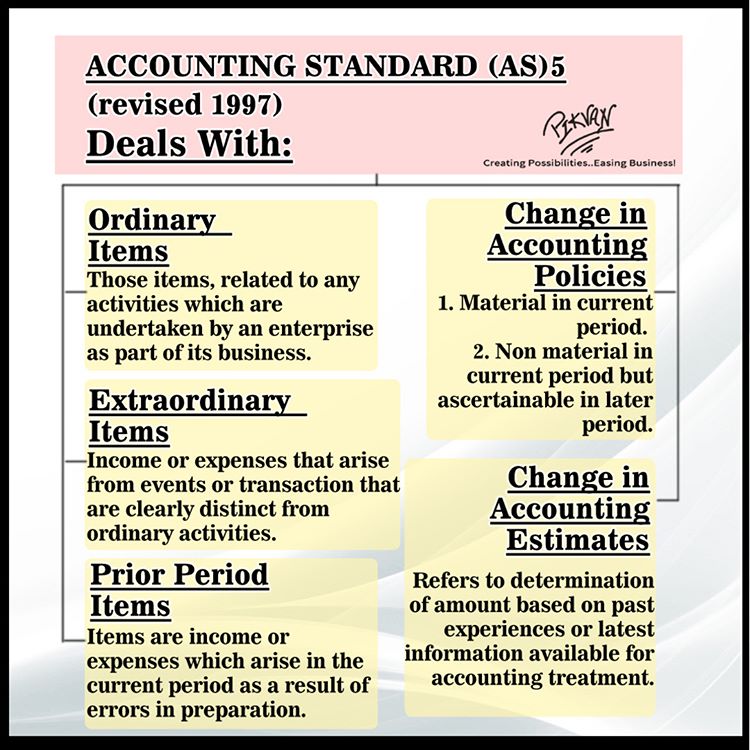

What is as 5 change in accounting policy

The objective of AS 5: Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies, is to prescribe the classification and disclosure of certain items in the statement of profit and loss so that all enterprises prepare and present such a statement on a uniform basis.

What is accounting standard 4

Ans: As per AS 4, adjustments to assets and liabilities are required for events occurring after the balance sheet date that provide additional information materially affecting the determination of the amounts relating to conditions existing at the balance sheet date.

What is IFRS 5 in accounting

IFRS 5 Non-current Assets Held for Sale and Discontinued Operations outlines how to account for non-current assets held for sale (or for distribution to owners).

What does IFRS 5 stand for

IFRS 5 refers to the International Financial Reporting Standards relating to Non-current assets held for sale and discontinued operations.

What is accounting standards 7

AS 7 Construction Contract describes and lays out the accounting treatment in respect of the revenue and costs in relation to a construction contract. AS 7 Construction Contract is to be used in for the accounting of construction contracts in the financial statements of the contractors.

What does accounting standard 7 mean

Accounting Standard 7 (AS 7) relates with accounting of construction contracts. The very purpose of this accounting standard is to specify the accounting treatment of revenue and costs associated with construction contracts.

What is the 5th steps on the accounting cycle

Defining the accounting cycle with steps: (1) Financial transactions, (2) Journal entries, (3) Posting to the Ledger, (4) Trial Balance Period, and (5) Reporting Period with Financial Reporting and Auditing.

What is accounting standard 10

The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of the financial statements can discern information about investment made by an enterprise in its property, plant and equipment and the changes in such investment.

What is accounting standard 3

Accounting Standard 3 deals with cash flow statement. This accounting standard accounts for information about changes in cash and cash equivalents of an entity during a particular period.

What are the 5 elements of IFRS

This chapter describes the objective and scope of financial statements and provides a description of the reporting entity. This chapter defines the five elements of financial statements—an asset, a liability, equity, income and expenses.

What is the objective and scope of IFRS 5

Objective of IFRS 5

IFRS 5 focuses on 2 main areas: It specifies the accounting treatment for assets (or disposal groups) held for sale, and. It sets the presentation and disclosure requirements for discontinued operations.

What does IFRS 5 deals with

IFRS 5 deals with the accounting for non-current assets held-for-sale, and the presentation and disclosure of discontinued operations.

What does IFRS 5 apply to

The IFRS shall be applied prospectively to non-current assets (or disposal groups) that meet the criteria to be classified as held for sale and operations that meet the criteria to be classified as discontinued after the effective date of the IFRS.

What is accounting standards 9

Accounting standard 9 is concerned with the recognition of revenue arising in the course of the. ordinary activities of the enterprise from: · From sale of goods, · From rendering of services, and. · From the use by others of enterprise resources yielding interest, royalties and dividends.

What is accounting standard 8 for

8 Ind ASs set out accounting policies that result in financial statements containing relevant and reliable information about the transactions, other events and conditions to which they apply. Those policies need not be applied when the effect of applying them is immaterial.

What are the 5 principles of an accountant 4 explain

Although the guidelines for accountants are extensive, there are five main principles that underpin accounting practices and the preparation of financial statements. These are the accrual principle, the matching principle, the historic cost principle, the conservatism principle and the principle of substance over form.

What are the 5 main activities involving accounting

The five main activities involved in accounting are gathering financial information, preparing and collecting permanent records, rearranging, summarizing, and classifying financial information, preparing information reports and summaries, and establishing controls to promote accuracy and honesty among employees.

What is accounting standard 11

❖ AS 11 deals with. ✓ Accounting for transactions in foreign currencies; ✓ Translating financial statements of foreign operations to reporting currency; and. ✓ Accounting for foreign currency transactions in the nature of forward.

What is accounting standard 7

Accounting Standard 7 (AS 7) relates with accounting of construction contracts. The very purpose of this accounting standard is to specify the accounting treatment of revenue and costs associated with construction contracts.

What is the meaning of IFRS 5

IFRS 5 refers to the International Financial Reporting Standards relating to Non-current assets held for sale and discontinued operations.

What is IFRS 5 summary

IFRS 5 became effective on January 1 2005, and has two main areas of focus: It specifies the accounting treatment for assets (or disposal groups) held for sale, and. It sets the presentation and disclosure requirements for discontinued operations.

What is the summary of IFRS 5

Summary. Under IFRS 5, a discontinued operation may be presented as a single line item within the statement of profit or loss and other comprehensive income or an entire separate column, detailed line by line. If the former approach is taken, a disclosure note must present a more detailed analysis.

Why is IFRS 5 important

Overall, IFRS 5 aims to provide transparency and useful information to the users of financial statements regarding an entity's decision to sell an asset or to discontinue some part of its business.